Financial Agents Need a HarnessAugust 3, 2026

READ MORE.svg)

Our General Counsel TuongVy Le wrote an opinion piece published in American Banker today about what happens when the default nature of money changes — how it’s held, the way it can be made productive — and what that means for banks and other businesses that have historically taken idle balances for granted.

For decades, customers have accepted that money sitting in an account earns little to nothing in exchange for safety, liquidity, and convenience. When moving money is hard, leaving it idle is tolerable. When deploying capital requires effort, many people don’t do it.

Stablecoins, tokenization, and onchain infrastructure like vaults are upending this structure. When assets are programmable, they can be deployed automatically, earn continuously, and the rules around them (lockups, permissions, redemption) can be enforced in code. That changes the default behavior of money.

The implication for banks is not abstract. Deposits have been cheap funding in part because customers tolerated below-market yields on idle balances. As that tolerance erodes, the first assets to move will be the ones banks care most about: large, sophisticated, mobile capital.

We’ve seen this movie before: When money market funds disrupted deposits, online brokerages made consumers question trading fees. Fintechs reimagined the customer payments experience. Each time, incumbents underestimated the shift until customer expectations had already changed.

Onchain assets and infrastructure are the next version of this pattern. This time, it represents a more seismic shift. The policy question for regulators is important. Right now, there’s a real asymmetry: Onchain systems are delivering value to consumers through products that generate continuous, programmatic yield, while banks are constrained in how they can custody and deploy assets. Allowing banks to remain competitive means the OCC must seriously engage with how onchain infrastructure and DeFi can be accessed safely: understanding who has control, what actions are possible, what constraints are enforceable, and how user protections are actually achieved.

The window for banks and their regulators to recognize and take advantage of the competitive opportunity is open, but not indefinitely.

Read the article here: American Banker

April 2026

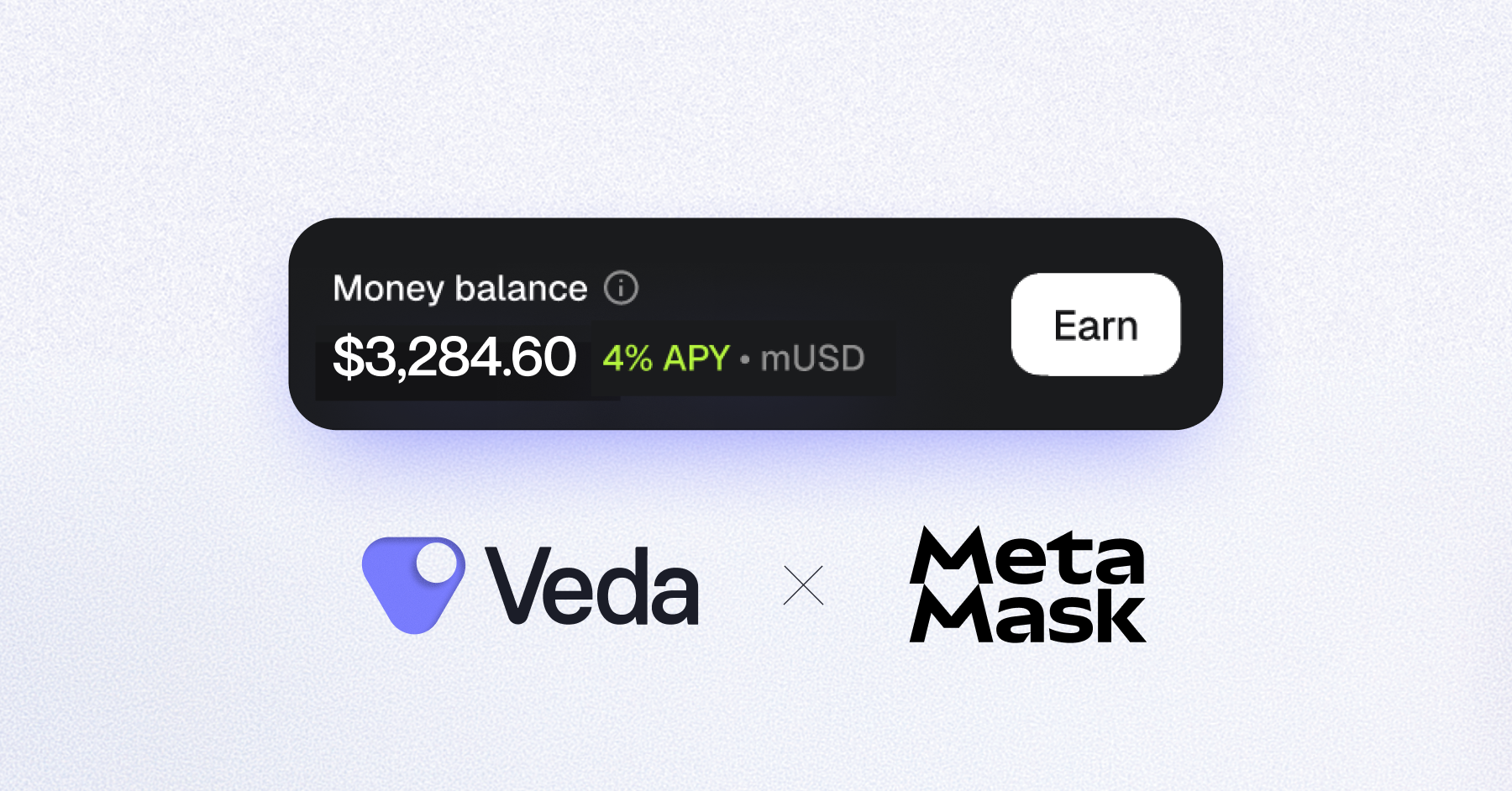

Digital asset infrastructure is reshaping consumer expectations.

Our General Counsel TuongVy Le wrote an opinion piece published in American Banker today about what happens when the default nature of money changes — how it’s held, the way it can be made productive — and what that means for banks and other businesses that have historically taken idle balances for granted.

For decades, customers have accepted that money sitting in an account earns little to nothing in exchange for safety, liquidity, and convenience. When moving money is hard, leaving it idle is tolerable. When deploying capital requires effort, many people don’t do it.

Stablecoins, tokenization, and onchain infrastructure like vaults are upending this structure. When assets are programmable, they can be deployed automatically, earn continuously, and the rules around them (lockups, permissions, redemption) can be enforced in code. That changes the default behavior of money.

The implication for banks is not abstract. Deposits have been cheap funding in part because customers tolerated below-market yields on idle balances. As that tolerance erodes, the first assets to move will be the ones banks care most about: large, sophisticated, mobile capital.

We’ve seen this movie before: When money market funds disrupted deposits, online brokerages made consumers question trading fees. Fintechs reimagined the customer payments experience. Each time, incumbents underestimated the shift until customer expectations had already changed.

Onchain assets and infrastructure are the next version of this pattern. This time, it represents a more seismic shift. The policy question for regulators is important. Right now, there’s a real asymmetry: Onchain systems are delivering value to consumers through products that generate continuous, programmatic yield, while banks are constrained in how they can custody and deploy assets. Allowing banks to remain competitive means the OCC must seriously engage with how onchain infrastructure and DeFi can be accessed safely: understanding who has control, what actions are possible, what constraints are enforceable, and how user protections are actually achieved.

The window for banks and their regulators to recognize and take advantage of the competitive opportunity is open, but not indefinitely.

Read the article here: American Banker

.webp)