Financial Agents Need a HarnessAugust 3, 2026

READ MORE.svg)

Learnings from the Tokenized podcast, based on a conversation between Veda CEO and Co-Founder Sunand Raghupathi, Tempo GTM Lead Simon Taylor, and Visa Head of Crypto Cuy Sheffield.

Everyone involved in blockchain product integration and regulation needs to understand the building blocks of our industry and the key terms that define it.

But something strange is happening in financial policy circles: Drafts of regulation are circulating that reference "staking stablecoins," a concept that doesn't exist.

Cuy Sheffield, head of crypto at Visa, explained the issue on an episode of the Tokenized podcast:

"I've literally seen in policy discussions, I have drafts of things that say you can stake a stablecoin. You can't stake a stablecoin."

This isn't a minor semantic issue. DeFi yield products are moving from crypto-native platforms into mainstream financial services: Kraken recently launched multi-protocol yield vaults with Veda, Coinbase has Morpho-based earn products, and Bitwise acquired a staking firm with $2.2 billion in assets.

Uniform vocabulary is important, but regulators are confused. Traditional finance professionals are confused. Even some builders may be confused.

So let's fix that.

DeFi yield can come from many different strategies, like staking, lending, looping, arbitrage, or other methods. Staking and lending are two of the most well-known yield strategies, but they come from fundamentally different sources. They share one thing in common: Both let you earn on your assets.

Staking is about supporting network security. When you stake ETH, SOL, or another proof-of-stake asset, you're locking up that asset to help validate transactions on that token's associated blockchain. In exchange, you earn fees as rewards.

“Staking has always been this entry point into DeFi,” Veda CEO and Co-Founder Sun Raghupathi explained on the Tokenized podcast.

When tokens are staked, the yield comes from transaction fees paid by network users and block rewards issued by the chain. Essentially, you're earning a share of the network's revenue by helping run it.

The key insight: Staking only works with the native asset of a proof-of-stake blockchain. You stake ETH to help secure Ethereum. You stake SOL to help secure Solana. You can’t stake BTC because the bitcoin blockchain doesn’t use a proof-of-stake mechanism to process transactions.

Similarly, you can’t stake a stablecoin because stablecoins don't secure networks. They're not the native asset of any proof-of-stake chain, so staking stablecoins is impossible.

The user for staking products already holds crypto and wants to earn yield on idle crypto assets they own.

Lending is about supplying capital. You deposit assets (including stablecoins) into a protocol, borrowers pay interest to access that capital, and you earn yield.

In DeFi lending, borrowers typically post crypto assets as collateral — often at 150% or more of the loan value — and pay interest to borrow stablecoins against those holdings. The yield lenders earn comes directly from the borrower's interest.

Protocols like Aave and Morpho facilitate this matching, though they differ materially in liquidity profiles and risk characteristics.

Raghupathi noted on the podcast:

Lending opens DeFi yield to "mainstream consumers who come across a stablecoin. They're not interested in crypto assets, but they want dollars, and they want to earn 3%, 4%, 8% on their dollars."

The customer for lending products may have never touched crypto before. They just want better returns on their dollars than what they might find with a high-interest savings account or traditional bank account.

If staking and lending are the raw ingredients for yield, vaults are the finished product and the vehicle that facilitates easy and transparent user access to those yield strategies.

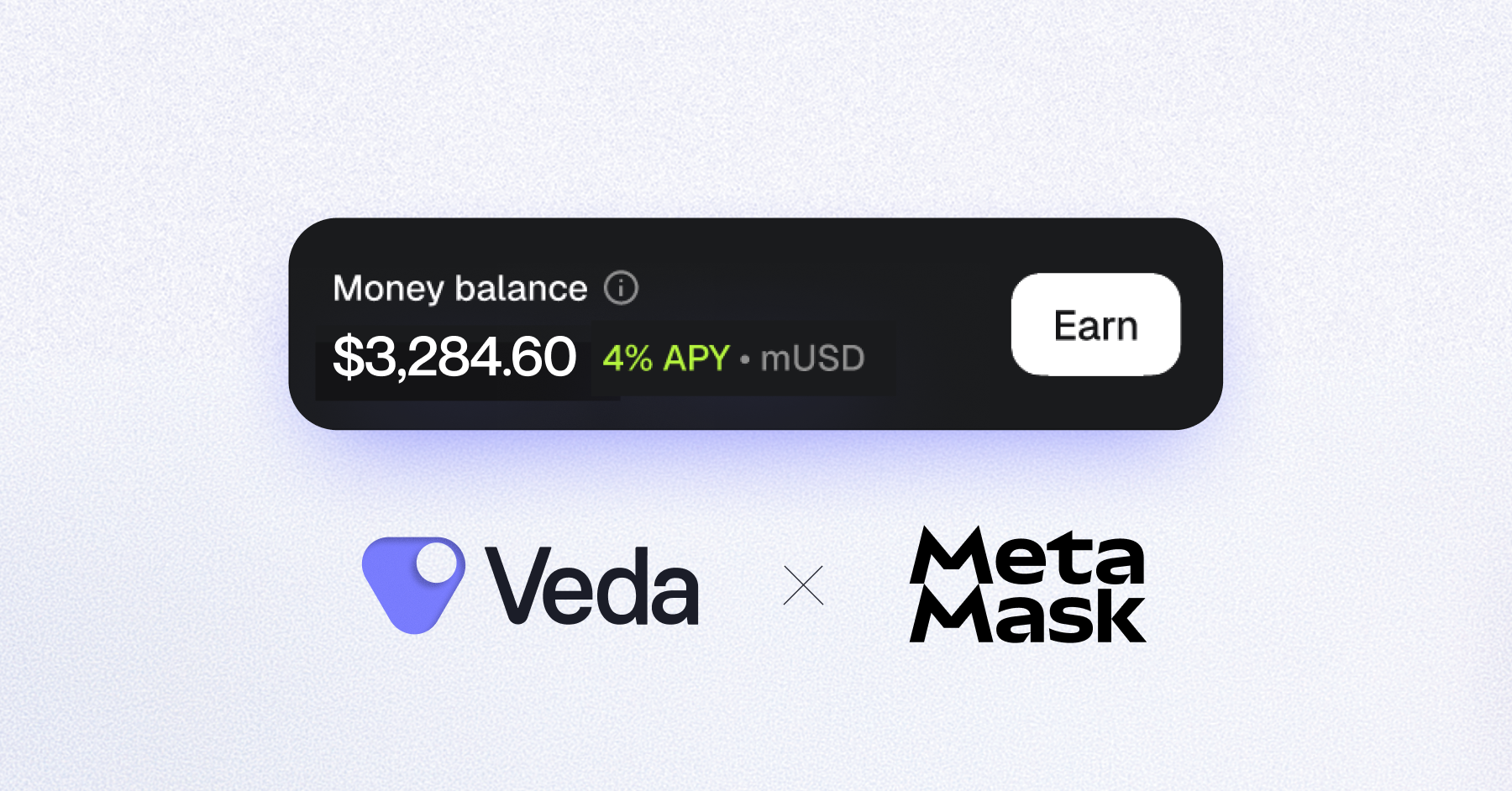

Veda’s vaults can aggregate yield across multiple protocols, yield strategies, and blockchains to go beyond just lending on a single protocol to offer a simplified experience with deeper liquidity and higher yield. The user deposits assets. The vault handles everything else — moving capital to wherever the best risk-adjusted yield is available.

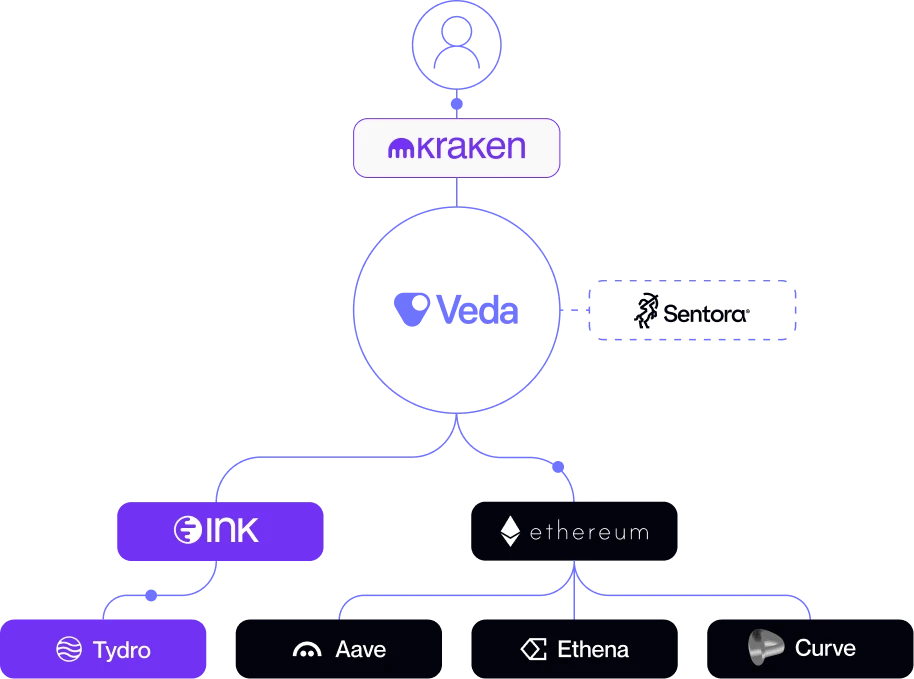

Kraken's new DeFi Earn product is an example of this. A Kraken Exchange user who may have never used DeFi directly before can deposit USDC and immediately start earning yield sourced from Aave, Morpho, Curve, and other protocols across multiple chains (in this case, across Ink and Ethereum).

The user doesn't need to know what any of those protocols are. They don't need to manage gas fees or bridge assets between chains. They aren’t limited to yields from just one protocol. They see an APY, with the ability to view other information like the current protocols used, associated fees, and the total value locked in the vault, and choose whether to participate.

For Kraken, Veda vaults provide the ultimate flexibility. Veda's vault technology allows for multichain liquidity and enables the ability to add or remove DeFi protocols as needed to adapt to changing market conditions.

Within its first week, Kraken's product attracted over $40 million in deposits (TVL) and 13,000 unique users — many of whom may have been accessing DeFi for the first time.

This is where traditional finance professionals might get stuck. A vault might sound like a fund or a structured product. In some ways, the mental model is similar. But the underlying mechanics are fundamentally different.

Three core features make vaults unique:

1. Transparency

All money movement happens onchain. Users can see exactly where their assets are at any moment. Unlike quarterly NAV reporting or delayed disclosure, vault positions are publicly verifiable in real-time. Users can also see how much money is in each vault and which protocols are being used to generate yield at any given time.

Raghupathi explains:

"A vault provides guarantees to users. They can see where their assets are at all times. It's all on the blockchain. It's all transparent. It's all publicly verifiable."

2. Cryptographic Constraints

Veda vaults operate under programmatic rules that limit what can happen to user assets by using an allowlist-only approach by default. This allows vaults to be compliant with existing laws and best practices and exist as an extra safeguard between the user and the DeFi protocol. Think of it as investment policy guidelines, enforced by code.

Controls on leverage, restrictions on which protocols can receive capital, limits on asset exposure — all of this is encoded in smart contracts and publicly auditable.

As Raghupathi puts it:

"They have guarantees as to what can happen to those assets. Things like control on leverage, what protocols can be taken out, what assets can this vault actually take exposure to — all of this stuff is all public. It's all verifiable onchain."

3. Non-Custodial Access

Users retain the ability to withdraw their assets at all times, without waiting on a fund manager who may or may not give them access when they need it.

This last point matters more than it might seem. The 2022 collapse of centralized yield platforms like Celsius and BlockFi demonstrated what happens when users can't verify where their assets are and can't access them on demand. The product concept — high-yield savings on stablecoins and crypto — was undeniably appealing. The architecture was the problem.

Raghupathi explains:

"People wanted high-yield savings accounts on their stablecoins. It's why those products did so well until they blew up. But why did they blow up? It's because there was no accountability. Customers couldn't see where their capital was. They didn't have access to their capital at all times."

Vaults are designed to solve exactly that problem in an onchain and compliant way.

If vaults are the product, curators are the professionals who manage them. They decide which protocols receive capital, how allocations shift over time, and how to balance yield against risk.

For Kraken's vaults, the curators are Chaos Labs and Sentora. They're specialized entities making active allocation decisions at the smart contract and protocol economics level.

Veda's vault infrastructure supports one or more curators per vault if desired. Veda vaults allow curators to change DeFi protocol allocations, plug into multiple protocols per vault, add or remove supported chains, change deposit assets, and modify yield strategies to ensure the best risk-adjusted yield is being delivered to users at all times.

So why not just call vault curators asset managers? Cuy Sheffield raised this question on the podcast:

"We've mentioned the term curator four times, and everyone's like, what is a curator? In my mind, I just default to asset manager."

Raghupathi's answer was nuanced: The competencies are similar. Both involve risk management on behalf of customers. The difference is how that relationship is mediated. Traditional asset managers operate in a trust-based relationship with clients. Curators operate under the cryptographic constraints described above, making their actions publicly verifiable. They're performing similar functions — risk management, capital allocation — but the accountability mechanism is fundamentally different. Users can verify rather than trust.

And the curator landscape is evolving quickly. Today's curators are crypto-native firms Raghupathi described as "the Steakhouses, the Sentoras and Chaoses" who built their expertise from the ground up. But that's already changing.

"What we're seeing is massive interest from traditional institutions to bring their risk management abilities onchain," Raghupathi notes. "We're going to see a fusion of these roles: asset managers, risk managers, and curators. We're all talking about the same thing, and these things will converge.”

For traditional financial institutions looking to enter onchain yield markets, there's been a clear progression of involvement:

Step 1: Staking

The entry point. Staking is well-understood, has mature infrastructure, and customers grasp the concept intuitively. Bitwise's acquisition of staking firm Chorus One, with its $2.2 billion in staked assets, is a recent example of asset managers moving into this space.

Step 2: Onchain Lending

Lending is a simple activity with clear parallels to traditional finance. Institutions are now getting educated on protocol mechanics, security considerations, and withdrawal dynamics.

Step 3: General-Purpose Vaults

The end state: Products that can access the full universe of onchain yield — staking, lending, RWAs, fixed income — all packaged into single offerings with appropriate risk controls. Flexible vault infrastructure, like what Veda offers with the BoringVault, makes it possible for enterprises to deploy vaults once and modify yield strategies, curators, blockchains, and protocols over time to adapt to evolving markets.

As Raghupathi puts it:

"This is a wave that is washing over all traditional institutions and all asset managers. It's a question of when and not if."

DeFi yield is entering a new phase, where the products are maturing, the infrastructure is scaling, and major exchanges are shipping real products to millions of users.

But confusion around terminology persists. It's important to understand core terms because regulators writing rules need to understand what they're regulating. Financial institutions evaluating opportunities need to know what they're buying. And depositors need to understand what they're using.

Staking secures networks. Lending supplies capital. Vaults aggregate yield across these and other yield strategies. Curators manage risk under cryptographic constraints.

These are the building blocks of onchain finance.

February 2026

How vaults power staking, lending, and so much more.

Learnings from the Tokenized podcast, based on a conversation between Veda CEO and Co-Founder Sunand Raghupathi, Tempo GTM Lead Simon Taylor, and Visa Head of Crypto Cuy Sheffield.

Everyone involved in blockchain product integration and regulation needs to understand the building blocks of our industry and the key terms that define it.

But something strange is happening in financial policy circles: Drafts of regulation are circulating that reference "staking stablecoins," a concept that doesn't exist.

Cuy Sheffield, head of crypto at Visa, explained the issue on an episode of the Tokenized podcast:

"I've literally seen in policy discussions, I have drafts of things that say you can stake a stablecoin. You can't stake a stablecoin."

This isn't a minor semantic issue. DeFi yield products are moving from crypto-native platforms into mainstream financial services: Kraken recently launched multi-protocol yield vaults with Veda, Coinbase has Morpho-based earn products, and Bitwise acquired a staking firm with $2.2 billion in assets.

Uniform vocabulary is important, but regulators are confused. Traditional finance professionals are confused. Even some builders may be confused.

So let's fix that.

DeFi yield can come from many different strategies, like staking, lending, looping, arbitrage, or other methods. Staking and lending are two of the most well-known yield strategies, but they come from fundamentally different sources. They share one thing in common: Both let you earn on your assets.

Staking is about supporting network security. When you stake ETH, SOL, or another proof-of-stake asset, you're locking up that asset to help validate transactions on that token's associated blockchain. In exchange, you earn fees as rewards.

“Staking has always been this entry point into DeFi,” Veda CEO and Co-Founder Sun Raghupathi explained on the Tokenized podcast.

When tokens are staked, the yield comes from transaction fees paid by network users and block rewards issued by the chain. Essentially, you're earning a share of the network's revenue by helping run it.

The key insight: Staking only works with the native asset of a proof-of-stake blockchain. You stake ETH to help secure Ethereum. You stake SOL to help secure Solana. You can’t stake BTC because the bitcoin blockchain doesn’t use a proof-of-stake mechanism to process transactions.

Similarly, you can’t stake a stablecoin because stablecoins don't secure networks. They're not the native asset of any proof-of-stake chain, so staking stablecoins is impossible.

The user for staking products already holds crypto and wants to earn yield on idle crypto assets they own.

Lending is about supplying capital. You deposit assets (including stablecoins) into a protocol, borrowers pay interest to access that capital, and you earn yield.

In DeFi lending, borrowers typically post crypto assets as collateral — often at 150% or more of the loan value — and pay interest to borrow stablecoins against those holdings. The yield lenders earn comes directly from the borrower's interest.

Protocols like Aave and Morpho facilitate this matching, though they differ materially in liquidity profiles and risk characteristics.

Raghupathi noted on the podcast:

Lending opens DeFi yield to "mainstream consumers who come across a stablecoin. They're not interested in crypto assets, but they want dollars, and they want to earn 3%, 4%, 8% on their dollars."

The customer for lending products may have never touched crypto before. They just want better returns on their dollars than what they might find with a high-interest savings account or traditional bank account.

If staking and lending are the raw ingredients for yield, vaults are the finished product and the vehicle that facilitates easy and transparent user access to those yield strategies.

Veda’s vaults can aggregate yield across multiple protocols, yield strategies, and blockchains to go beyond just lending on a single protocol to offer a simplified experience with deeper liquidity and higher yield. The user deposits assets. The vault handles everything else — moving capital to wherever the best risk-adjusted yield is available.

Kraken's new DeFi Earn product is an example of this. A Kraken Exchange user who may have never used DeFi directly before can deposit USDC and immediately start earning yield sourced from Aave, Morpho, Curve, and other protocols across multiple chains (in this case, across Ink and Ethereum).

The user doesn't need to know what any of those protocols are. They don't need to manage gas fees or bridge assets between chains. They aren’t limited to yields from just one protocol. They see an APY, with the ability to view other information like the current protocols used, associated fees, and the total value locked in the vault, and choose whether to participate.

For Kraken, Veda vaults provide the ultimate flexibility. Veda's vault technology allows for multichain liquidity and enables the ability to add or remove DeFi protocols as needed to adapt to changing market conditions.

Within its first week, Kraken's product attracted over $40 million in deposits (TVL) and 13,000 unique users — many of whom may have been accessing DeFi for the first time.

This is where traditional finance professionals might get stuck. A vault might sound like a fund or a structured product. In some ways, the mental model is similar. But the underlying mechanics are fundamentally different.

Three core features make vaults unique:

1. Transparency

All money movement happens onchain. Users can see exactly where their assets are at any moment. Unlike quarterly NAV reporting or delayed disclosure, vault positions are publicly verifiable in real-time. Users can also see how much money is in each vault and which protocols are being used to generate yield at any given time.

Raghupathi explains:

"A vault provides guarantees to users. They can see where their assets are at all times. It's all on the blockchain. It's all transparent. It's all publicly verifiable."

2. Cryptographic Constraints

Veda vaults operate under programmatic rules that limit what can happen to user assets by using an allowlist-only approach by default. This allows vaults to be compliant with existing laws and best practices and exist as an extra safeguard between the user and the DeFi protocol. Think of it as investment policy guidelines, enforced by code.

Controls on leverage, restrictions on which protocols can receive capital, limits on asset exposure — all of this is encoded in smart contracts and publicly auditable.

As Raghupathi puts it:

"They have guarantees as to what can happen to those assets. Things like control on leverage, what protocols can be taken out, what assets can this vault actually take exposure to — all of this stuff is all public. It's all verifiable onchain."

3. Non-Custodial Access

Users retain the ability to withdraw their assets at all times, without waiting on a fund manager who may or may not give them access when they need it.

This last point matters more than it might seem. The 2022 collapse of centralized yield platforms like Celsius and BlockFi demonstrated what happens when users can't verify where their assets are and can't access them on demand. The product concept — high-yield savings on stablecoins and crypto — was undeniably appealing. The architecture was the problem.

Raghupathi explains:

"People wanted high-yield savings accounts on their stablecoins. It's why those products did so well until they blew up. But why did they blow up? It's because there was no accountability. Customers couldn't see where their capital was. They didn't have access to their capital at all times."

Vaults are designed to solve exactly that problem in an onchain and compliant way.

If vaults are the product, curators are the professionals who manage them. They decide which protocols receive capital, how allocations shift over time, and how to balance yield against risk.

For Kraken's vaults, the curators are Chaos Labs and Sentora. They're specialized entities making active allocation decisions at the smart contract and protocol economics level.

Veda's vault infrastructure supports one or more curators per vault if desired. Veda vaults allow curators to change DeFi protocol allocations, plug into multiple protocols per vault, add or remove supported chains, change deposit assets, and modify yield strategies to ensure the best risk-adjusted yield is being delivered to users at all times.

So why not just call vault curators asset managers? Cuy Sheffield raised this question on the podcast:

"We've mentioned the term curator four times, and everyone's like, what is a curator? In my mind, I just default to asset manager."

Raghupathi's answer was nuanced: The competencies are similar. Both involve risk management on behalf of customers. The difference is how that relationship is mediated. Traditional asset managers operate in a trust-based relationship with clients. Curators operate under the cryptographic constraints described above, making their actions publicly verifiable. They're performing similar functions — risk management, capital allocation — but the accountability mechanism is fundamentally different. Users can verify rather than trust.

And the curator landscape is evolving quickly. Today's curators are crypto-native firms Raghupathi described as "the Steakhouses, the Sentoras and Chaoses" who built their expertise from the ground up. But that's already changing.

"What we're seeing is massive interest from traditional institutions to bring their risk management abilities onchain," Raghupathi notes. "We're going to see a fusion of these roles: asset managers, risk managers, and curators. We're all talking about the same thing, and these things will converge.”

For traditional financial institutions looking to enter onchain yield markets, there's been a clear progression of involvement:

Step 1: Staking

The entry point. Staking is well-understood, has mature infrastructure, and customers grasp the concept intuitively. Bitwise's acquisition of staking firm Chorus One, with its $2.2 billion in staked assets, is a recent example of asset managers moving into this space.

Step 2: Onchain Lending

Lending is a simple activity with clear parallels to traditional finance. Institutions are now getting educated on protocol mechanics, security considerations, and withdrawal dynamics.

Step 3: General-Purpose Vaults

The end state: Products that can access the full universe of onchain yield — staking, lending, RWAs, fixed income — all packaged into single offerings with appropriate risk controls. Flexible vault infrastructure, like what Veda offers with the BoringVault, makes it possible for enterprises to deploy vaults once and modify yield strategies, curators, blockchains, and protocols over time to adapt to evolving markets.

As Raghupathi puts it:

"This is a wave that is washing over all traditional institutions and all asset managers. It's a question of when and not if."

DeFi yield is entering a new phase, where the products are maturing, the infrastructure is scaling, and major exchanges are shipping real products to millions of users.

But confusion around terminology persists. It's important to understand core terms because regulators writing rules need to understand what they're regulating. Financial institutions evaluating opportunities need to know what they're buying. And depositors need to understand what they're using.

Staking secures networks. Lending supplies capital. Vaults aggregate yield across these and other yield strategies. Curators manage risk under cryptographic constraints.

These are the building blocks of onchain finance.

.webp)